#130- Forward Deployment Index

The next billion dollar ARR company in AI will be forward deployed

The software arrives after the workflow changes

Many investments later we can confirm in large parts of enterprise AI, the software arrives after the workflow changes. That pattern increasingly appears across healthcare AI, industrial operations, insurance workflows, enterprise governance systems, defence, logistics, and infrastructure management. Companies initially enter the market looking like software vendors. A few quarters later, they resemble deployment organizations sitting directly inside customer operations.

Several enterprise AI startups now spend more on deployment engineering, workflow implementation, and operational integration than on model development during their first 24 months. This shift matters because it changes where value accrues in enterprise AI.

The bottleneck shifted from models to organizations

Most large enterprises already have access to frontier models. OpenAI, Anthropic, Gemini, open source systems, fine tuned variants, retrieval stacks, and copilots are no longer difficult to procure. The bottleneck increasingly sits elsewhere. Enterprise AI adoption is constrained by organizational redesign capacity.

Most enterprises do not lack AI access. They lack internal agreement on how decisions should change once AI enters the workflow. A company deploying AI into underwriting, radiology, procurement, compliance, manufacturing, or infrastructure operations is rarely inserting software into a stable workflow. The workflow itself changes during deployment. That distinction explains why so many enterprise AI deployments stall after successful pilots.

Traditional enterprise software standardized workflows organizations already understood. A company implementing CRM software already knew how lead routing, approvals, account ownership, and sales reporting worked. ERP systems digitized procurement hierarchies, inventory systems, reconciliation rules, and financial controls that already existed operationally.

AI changes operational decision structures themselves.

A hospital deploying radiology copilot has to determine acceptable confidence thresholds, escalation ownership, auditability standards, human review frequency, liability boundaries, and downstream accountability. Industrial companies deploying AI inspection systems often discover that defect classification standards differ materially across plants despite supposedly standardized operating procedures.

These are organizational reconstruction problems before they become software problems.

McKinsey’s 2025 enterprise AI survey showed that most organizations now report AI adoption in at least one business function.

Yet only a small minority report material enterprise wide EBIT impact. The deployment bottleneck increasingly appears less related to model access and more related to operational integration.

AI deployments now require cross-functional operational alignment

What makes this harder than previous software transitions is that enterprise AI deployments frequently force coordination across functions that historically operated independently. Compliance, operations, legal, procurement, IT, and frontline workflow owners now have to jointly define escalation paths, override conditions, auditability standards, and acceptable failure rates before deployment stabilizes. In many organizations, these groups rarely shared operational ownership before AI entered the system.

That coordination burden is becoming one of the defining variables in enterprise AI adoption.

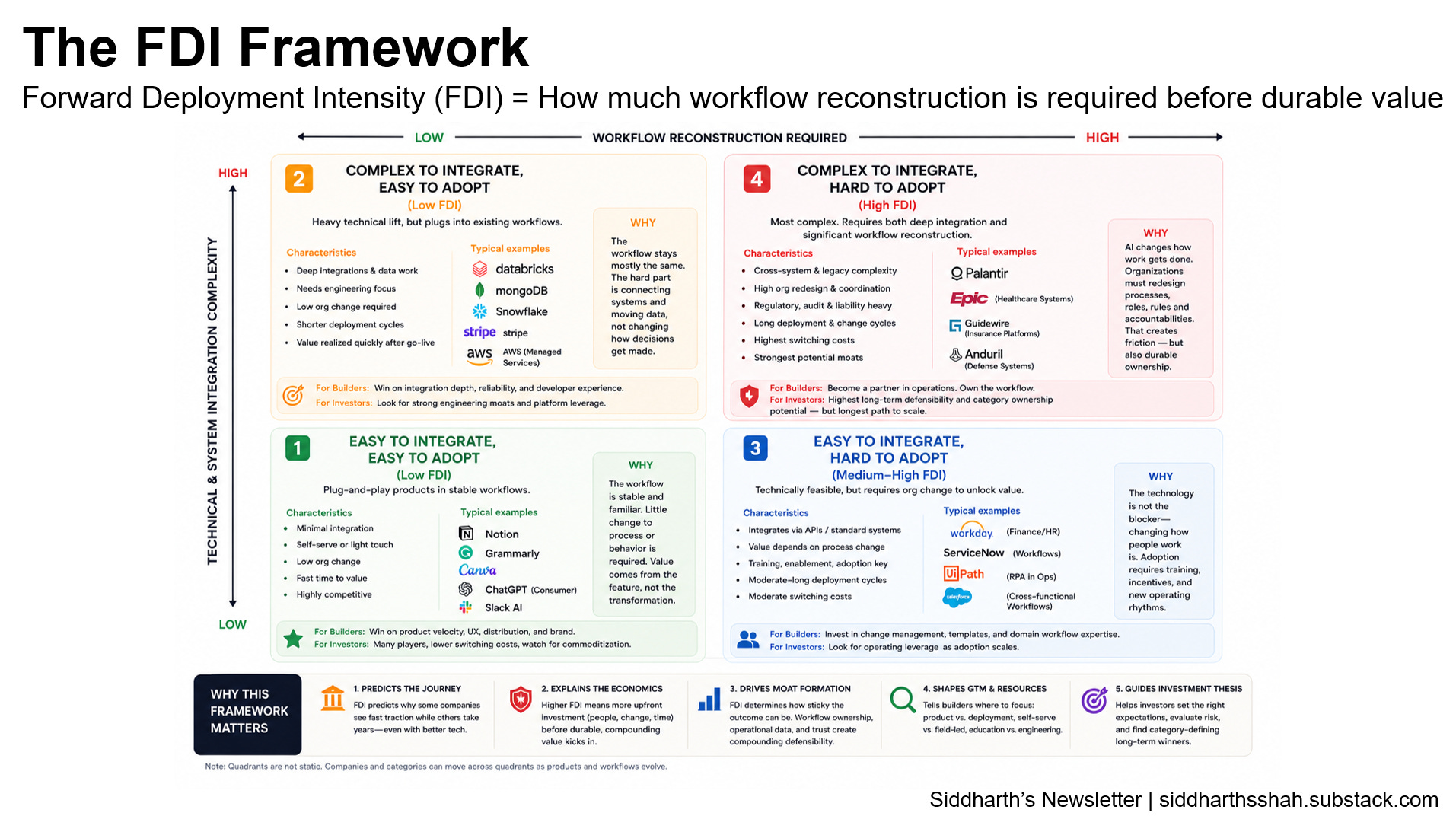

Forward Deployment Intensity (FDI)

This creates a useful framework for analyzing enterprise AI companies: Forward Deployment Intensity, or FDI. FDI measures how much workflow reconstruction must happen before recurring software revenue becomes durable. At a practical level, FDI rises when deployments require extensive workflow redesign across multiple systems, dense exception handling, frequent human overrides, regulatory coordination, long retraining cycles after deployment, and ongoing operational involvement from the vendor after implementation.

Low FDI categories include lightweight productivity tooling, note-taking systems, horizontal copilots, generic content generation, and broad workflow assistants. The software enters relatively stable workflows with limited organizational redesign.

High FDI categories include healthcare systems, industrial operations, enterprise governance, defence software, infrastructure management, utilities, manufacturing automation, and insurance operations. These deployments frequently require workflow reconstruction before the software itself becomes repeatable.

Why high FDI companies initially look unattractive

This distinction increasingly matters because many investors still evaluate both categories using nearly identical SaaS assumptions. And that likely produces systematic mispricing.

High FDI companies frequently look unattractive during years 1-3 because implementation labor appears before repeatability does. Gross margins compress early. Deployment teams scale before product teams stabilize. Services revenue rises before recurring software revenue matures. Customer concentration initially remains high because deployments are operationally intensive.

Traditional SaaS frameworks interpret many of these signals negatively. Yet these same companies may simultaneously accumulate assets that are substantially harder to replicate later: workflow ownership, operational trust, deployment history, edge case datasets, escalation logic, audit systems, exception handling infrastructure, and organization-specific process knowledge.

Deployment learning compounds

The deployment phase itself increasingly behaves like proprietary data acquisition.

Every deployment improves routing logic. Every edge case improves evaluation systems. Every escalation improves workflow reliability. Every regulated environment improves auditability. Over time, the company accumulates operational knowledge that generalized software vendors cannot easily reproduce through model access alone.

That operational learning compounds.

This may ultimately become one of the defining economic differences between low FDI and high FDI AI markets.

Low FDI categories may remain structurally competitive because model capability diffuses quickly, switching costs remain limited, and workflow reconstruction burdens stay low. Product velocity and distribution likely dominate outcomes.

High FDI markets may concentrate much more aggressively over time. High FDI markets may resemble defence, infrastructure, or systems markets more than traditional SaaS markets.

The company that processes 10 million insurance edge cases, industrial defects, radiology exceptions, infrastructure incidents, or enterprise governance escalations may accumulate operational knowledge that becomes increasingly difficult for later entrants to replicate quickly. The deployment history itself improves future deployments. The workflow knowledge improves implementation speed. The audit structures improve reliability. The edge case corpus improves automation quality.

The moat increasingly sits inside the workflow.

Enterprise AI may invert traditional SaaS assumptions

For the last 15 years, software markets generally rewarded standardization. Low implementation burden, rapid onboarding, minimal services intensity, and high gross margins often signaled product quality.

Enterprise AI may partially invert those assumptions in high FDI markets.

Implementation heavy companies may initially look operationally messy precisely because they are accumulating deployment learning that later strengthens workflow ownership. Services intensity during early deployment phases may correlate positively with long-term defensibility in regulated or operationally complex categories.

That does not mean every services heavy AI company becomes durable software. Many will remain implementation firms with limited repeatability.

The important distinction is whether deployment learning converts into standardized operational infrastructure over time.

The org chart increasingly reveals more than the demo

This also explains a hiring pattern that still appears underappreciated across much of venture investing.

Several enterprise AI startups are now hiring forward deployed engineers, workflow architects, implementation specialists, evaluation teams, human in the loop QA teams, policy operators, and domain specific deployment staff earlier than traditional SaaS companies typically would. In some sectors, deployment engineering headcount now scales faster than core product engineering during early commercialization phases.

The organizational chart increasingly reveals more than the product demo. That operating structure increasingly appears across enterprise AI, particularly in regulated or operationally complex sectors where reliability matters more than generalized software abstraction.

The next moat may sit inside the workflow

In high FDI markets, deployment learning may compound faster than model differentiation. The companies that control the workflow may ultimately control the category.